![[Translate to English:]](/fileadmin/redaktion/Fakultaeten/Wirtschaftswissenschaftliche_Fakultaet/DICE/Das_Team/Bilder_Mitarbeiter_254px/andre_romahn_cropped.jpg "[Translate to English:]")

By Jun.-Prof. Dr. Andre Romahn (Foto)

For competition authorities such as the German Federal Cartel Office or the European Commission, the assessment of mergers of competing companies is one of their core competences. The decision to be taken is not limited to the mere approval or rejection. Rather, it is also decided in which form or under which conditions an approval can be granted. The possibility to request specific commitments allows competition authorities to tailor a proposed merger in such a way that negative effects on end customers are minimized or avoided altogether. However, the formulation of such obligations is a challenge, especially in differentiated product markets.

In differentiated product markets, customers have dozens or often hundreds of products to choose from. The merger between the Carlsberg and Pripps breweries in Sweden in 2001 is a good example of this. At that time, the two breweries accounted for 26 and 17 per cent of sales in the Swedish beer market respectively. In total, the two breweries held 44 different beers in their combined product portfolio. The Swedish competition authority (Konkurrensverket) only approved the merger under the condition that a total of 12 beers with a 6 per cent share of sales were sold to the competitor Galatea. At that time, Galatea was a pure niche supplier with a market share of only 0.5 per cent.

The regression analysis by Friberg and Romahn (2015) concludes that the sale to Galatea will result in a price reduction of 3 per cent for the beers concerned. From an economic point of view, this effect can be explained by the fact that in differentiated product markets, companies develop market power through a portfolio of easily substitutable products, i.e. products that are perceived by buyers as similar. As a result of this market power, the prices of these products can be set higher compared to the products offered by different, competing companies. The reason for this is that if the price of a beer in the Carlsberg and Pripps portfolio increases, some customers will decide to buy another beer. This substitute will generally be very similar to the beer concerned. With a large portfolio of well substitutable beers, it is therefore likely that buyers who choose to buy another beer will nevertheless buy it from the same brewery. Thus, despite the price increase, competitors will not benefit and will not acquire new customers. As Galatea was a pure niche supplier, the acquisition of the beers from Carlsberg and Pripps enabled it to significantly increase its market share, but do not gain market power. Consequently, Galatea was not able to maintain the prices of the beers sold at pre-merger levels. Consumers benefit from this effect through falling prices.

In order to quantify the effect not only on the beers sold but also on the market as a whole, we have estimated a structural demand and supply model. With this model the new market equilibrium with the merged Carlsberg-Pripps brewery can be calculated. Our econometric results show that the divestments reduce the average price increase in the overall market by two thirds. Without divestments to competitors, the price increase of the remaining Carlsberg and Pripps beers would have been 87 and 33 per cent higher.

The remaining interesting question is whether the Swedish Competition Authority could have achieved even better results from a consumer perspective if another competitor had purchased the beers or if other beers had been sold to Galatea. In answering the first part of this question, it is not surprising that the price increase in the overall market would have been higher if the beers had been sold to a larger competitor. If Spendrups, the second largest remaining supplier in the market, had bought the beers and not Galatea, the average price increase in the market would have been twice as high. In answering the second part, the challenge is to determine an optimal set of beers to be divested. In the approved merger between Carlsberg and Pripps, 12 beers out of a total of 44 beers from the two companies were sold. If one really considers only one of the total of five competitors in the market to purchase the beers, 12 draws without putting aside out of 44 possible beers would result in a total of 21 billion possibilities. Even with the computing capacity available today, this total number is significantly higher than what appears to be justifiable as computing effort.

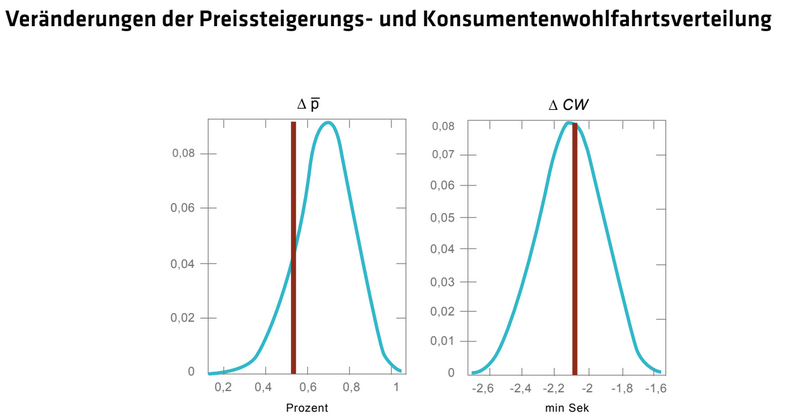

Many of the possible alternatives would also be impracticable to implement because they involve beers that neither Pripps nor Carlsberg would divest. In order to determine realistic alternative combinations of beers and to reduce the enormous computing load, we use a simple stochastic method. We determine that the total turnover of each possible combination lies within a window that represents a maximum of 10 per cent deviation up or down from the 6 per cent of total turnover set in the approved merger. In order to determine an alternative combination, we randomly select beers from the overall portfolio of Carlsberg and Pripps until the proportion of total sales is within the defined range. For each of these combinations we calculate the new market equilibrium with the merged Carlsberg-Pripps brewery. This gives statistical distributions for the average price increase and the total welfare loss caused by the merger. We generate counterfactual scenarios until the price increase and consumer welfare distributions remain statistically stable. This is already the case after 200,000 randomly selected combinations. The distributions can be seen in the chart.

{kind=link}

The vertical red line marks the result of the actually approved merger. Both distributions show that the portfolio of beers actually divested produces effects that are close to the median. Fears that Carlsberg and Pripps could influence the choice of beers in such a way as to maximise the price increase and thereby maximise the loss of consumer welfare are not borne out.

The vertical red line marks the result of the actually approved merger. Both distributions show that the portfolio of beers actually divested produces effects that are close to the median. Fears that Carlsberg and Pripps could influence the choice of beers in such a way as to maximise the price increase and thereby maximise the loss of consumer welfare are not borne out.

The merger of Carlsberg and Pripps in Sweden shows, on the one hand, that the imposition of product divestments to competitors is an effective means of reducing or preventing price increases caused by mergers. On the other hand, it shows that the effects of an apparently overwhelmingly high number of possible product divestments can be systematically analysed and quantified. Conditions on product divestitures for the approval of a merger between competitors are thus an effective tool in the toolbox of competition regulators.

This article is also published in the DICE Policy Brief.

DICE PUBLIKATION

Richard Friberg & Andre Romahn (2015), Divestiture Requirements as a Tool for Competition Policy: A Case from the Swedish Beer Market, International Journal of Industrial Organization 42, 1-18.